YieldMax Funds: The Illusion of High Dividends and the Reality of Losing Capital

At first glance, YieldMax funds look like a dream.

At first glance, YieldMax funds look like a dream.

You see:

-

Massive dividend yields

-

Monthly payouts (or even weekly)

-

Income streams that seem almost too good to be true

And for a lot of people—especially income-focused investors—it’s incredibly tempting.

The idea is simple:

“I can just collect these huge dividends and live off the income.”

But beneath that surface is a much harsher reality.

Because what looks like income is often something very different:

You’re getting paid back with your own money while the underlying asset quietly collapses.

The Appeal: Why YieldMax Funds Look So Attractive

YieldMax funds are designed to generate high income, often through options strategies like:

-

Covered calls

-

Synthetic positions

-

Derivatives tied to underlying stocks

On paper, this creates:

-

Extremely high yields

-

Frequent payouts

-

The appearance of steady income

And that’s where the hook is.

You might see:

-

40% yield

-

60% yield

-

Sometimes even higher

Compared to traditional investments:

-

3–5% dividend stocks

-

4–6% bonds

It feels like a no-brainer.

But that comparison is misleading.

The Core Problem: Yield Isn’t Profit

This is the most important concept to understand:

A high yield does not mean you’re making money.

Yield is just:

-

The amount being paid out

-

Relative to the current price

It says nothing about:

-

Total return

-

Capital preservation

-

Long-term performance

And in the case of many YieldMax funds, a large portion of that “yield” is actually:

Return of capital.

Return of Capital: The Hidden Mechanism

Return of capital means:

-

The fund is giving you back your own invested money

Not profits. Not earnings.

Your money.

So what happens over time?

-

You receive large payouts

-

Your account shows income

-

But the fund’s NAV (Net Asset Value) declines

It’s like taking money out of your own wallet and calling it income.

It feels good in the moment—but it’s not sustainable.

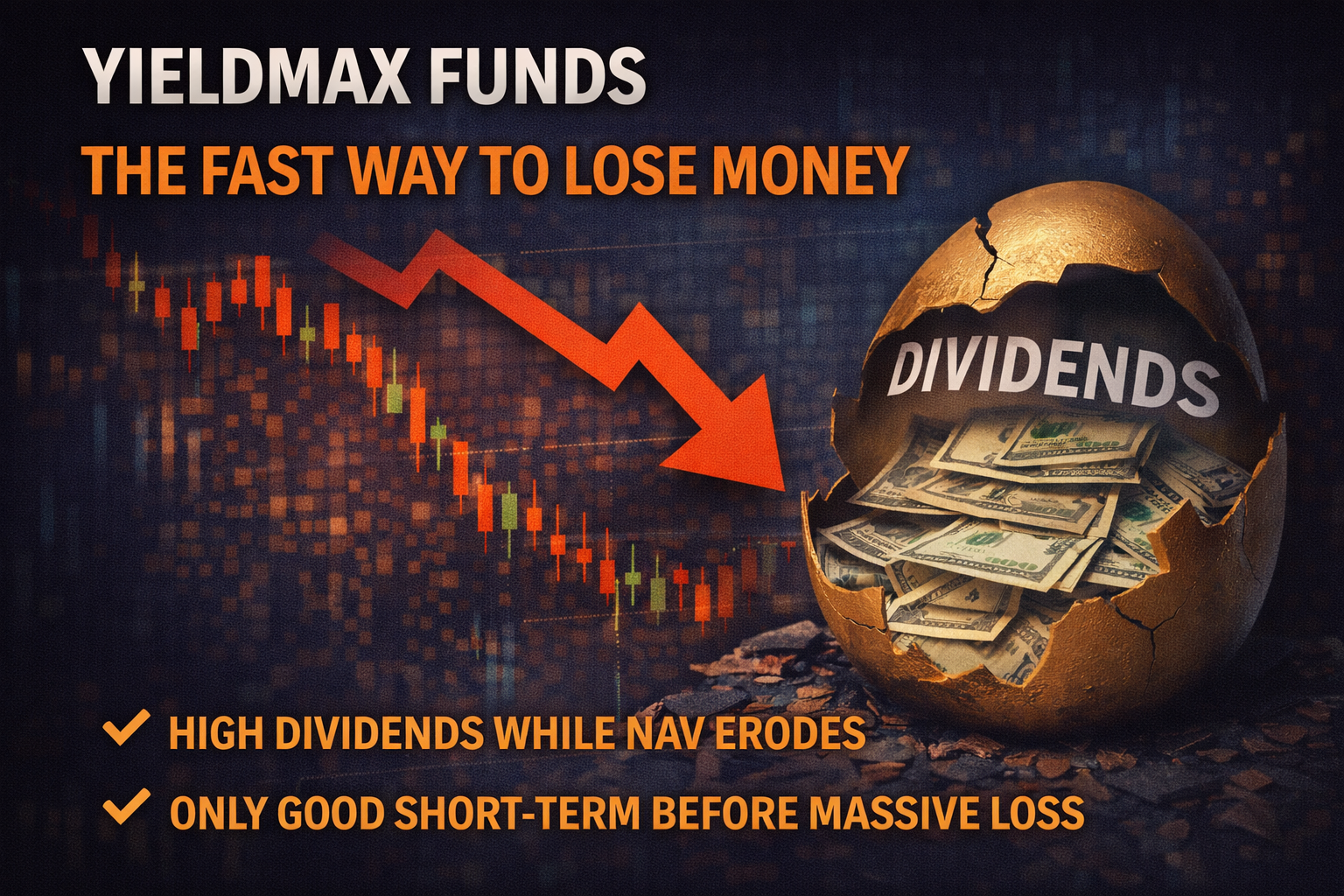

NAV Erosion: The Silent Killer

NAV erosion is the slow, consistent decline in the value of the fund itself.

With many YieldMax funds:

-

The price trends downward over time

-

Even as dividends are paid

So you might see:

-

$10 → $8 → $6 → $4 → $2

All while collecting “income.”

But when you zoom out, the reality becomes clear:

Your total value is shrinking.

The dividends aren’t compensating for the loss in price—they’re part of the reason for it.

Why This Happens

YieldMax funds rely heavily on options strategies.

While these can generate income, they also:

-

Cap upside potential

-

Expose the fund to downside risk

-

Depend on market conditions

When the underlying asset struggles:

-

The fund struggles

-

NAV declines

-

Income becomes harder to sustain

To maintain high payouts, the fund may:

-

Return capital

-

Reduce distributions

-

Adjust strategy

But the damage is already happening.

The Reverse Split Cycle

As NAV erodes, funds eventually face a problem:

Their share price becomes too low.

When that happens, they often perform a reverse split.

For example:

-

10 shares at $1 → 1 share at $10

On paper, nothing changes.

But in reality:

-

Dividend payouts are reduced

-

The cycle starts again

-

Long-term holders lose value

This is not a sign of strength.

It’s a sign of decline.

Dividend Cuts: The Inevitable Outcome

High yields are not stable.

Over time:

-

As NAV declines

-

As income generation weakens

Dividends get cut.

What started as:

-

50% yield

Becomes:

-

30%

-

Then 20%

-

Then lower

And now you’re left with:

-

A lower-paying fund

-

A much lower share price

-

A significant capital loss

The Case Study: ULTY

A real-world example makes this clearer.

Take a fund like ULTY.

Over roughly two years:

-

The share price has dropped around 83%

-

The dividend yield was cut by 47% in the first year

-

And is on pace for another ~50% reduction

So what does that mean in practice?

Even if you collected:

-

Large monthly dividends

Your overall position:

-

Lost significant value

Because the decline in price far outweighed the income received.

The Illusion of “Income Investing”

One of the biggest traps with YieldMax funds is psychological.

You see:

-

Cash hitting your account

-

Regular payouts

-

A sense of progress

It feels like:

“I’m making money.”

But if your total account value is going down, you’re not generating income.

You’re liquidating your own investment—slowly.

Short-Term vs Long-Term Reality

To be fair, YieldMax funds are not completely useless.

They can work in the short term.

If you:

-

Enter at the right time

-

Collect a few months of high payouts

-

Exit before significant NAV erosion

You can come out ahead.

But that requires:

-

Timing

-

Discipline

-

A clear exit plan

What doesn’t work is:

-

Buying and holding

-

Treating it like a traditional dividend investment

-

Assuming the yield will sustain itself

Because over time:

The math catches up.

The One-Year Danger Zone

A practical way to think about it:

-

Short-term (a few months): potential opportunity

-

Long-term (1+ year): high probability of loss

Why?

Because:

-

NAV erosion compounds

-

Dividend cuts accumulate

-

Total return turns negative

After a year, in many cases:

-

Even the dividends you collected

-

Won’t make up for the loss in share price

Why People Keep Falling for It

Despite all this, YieldMax funds remain popular.

Why?

Because they tap into powerful biases:

1. Yield Obsession

People focus on:

-

Percentage yield

Instead of:

-

Total return

A 50% yield sounds incredible—until you realize your capital is disappearing.

2. Immediate Gratification

Monthly payouts feel good.

They create:

-

Positive reinforcement

-

A sense of income

-

Emotional attachment

Even if the underlying investment is declining.

3. Misunderstanding of Dividends

Many investors assume:

-

Dividends = profit

But in these cases:

-

Dividends often = return of capital

That misunderstanding is costly.

What Real Income Investing Looks Like

Sustainable income investing is very different.

It focuses on:

-

Stable companies

-

Real earnings

-

Manageable payout ratios

-

Long-term growth

Yields are typically:

-

Lower

-

More realistic

-

Actually supported by cash flow

It’s not exciting.

But it’s real.

The Bottom Line

YieldMax funds are not magic income machines.

They are:

-

Complex financial products

-

Designed to generate high payouts

-

Often at the expense of long-term value

They can:

-

Look attractive

-

Feel profitable

-

Provide short-term gains

But over time, the pattern is clear:

-

NAV declines

-

Dividends get cut

-

Capital erodes

And many investors are left wondering:

“Where did my money go?”

Final Thoughts: Don’t Be Fooled by the Yield

High yield is one of the most seductive traps in investing.

It promises:

-

Easy income

-

Fast returns

-

Financial freedom

But when that yield is driven by:

-

Return of capital

-

Unsustainable strategies

-

Declining NAV

It’s not income.

It’s erosion.

So if you choose to trade YieldMax funds, treat them for what they are:

Short-term tools—not long-term investments.

Because if you hold them too long, the outcome is rarely surprising.

You collected the dividends.

But you lost the investment.